As we head into 2023, the Property & Casualty (P&C) insurance market faces a range of both challenges and opportunities. This year’s report anticipates shifting economic conditions, changing regulatory requirements, emerging risks such as cybercrimes, and most importantly, catastrophic events (CAT).

Just this past 2022, claims resulting from Hurricane Ian cost insurers billions in losses. According to USI National Practice Leaders’, “severe weather events, supply chain challenges, [and] an increased focus on ESG (exposure to environmental, social and governance risks) and inflationary pressures” will negatively disturb market capacity, coverage, and premiums.

As headwinds from economic conditions, social inflation, labor shortages, supply chain disruptions, and natural disasters mount concern for both consumers and insurers alike, it’s important to understand how the insurance marketplace in responding. Anticipating market trends by staying informed and partnering with a proactive agency partner will help improve outcomes for 2023. At HAWK Advisers, we strive to overcome these challenges by adopting industry best practices, keeping our customers informed, benchmarking carrier performance, merit-based negotiations, and identifying alternative carrier arrangements in the event of an unexpected change in terms and/or pricing.

What are some major challenges or implications? What are the impending threats for the insurance industry in 2023?

When it comes to the P&C insurance market, there are numerous liabilities and risks that directly affect policyholders. Simultaneously, insurers encounter their own set of challenges when trying to develop optimal coverage for businesses or individuals. With an increased demand for coverage and higher premiums, these areas of insurance are expected to impact or become further impacted in the 2023 market:

- Increased competition: With a large number of insurers targeting customers that fit their risk profiles, insureds are faced with numerous conflicting factors when differentiating between carriers, such as developing technologies, range of service, and price strategies. Equally, insurers are expected to keep up with fluctuating economic changes by diversifying their products and services as well as investing in technology to improve the insured’s experience and reduce cost.

- Cybersecurity risks: Reports of increasing cyber-attacks and harsher regulatory environments are hastening the need for cyber insurance. Unfortunately, insurers are becoming queasy as claims payment continue to rise on lines of coverage such as cyber extorsion, social engineering fraud, and electronic fund transfer fraud. Cyber carriers are responding by raising their cost for coverage, demanding network and data safeguarding, and reducing capacity. The cyber insurance market is changing rapidly and it’s expected to progressively harden throughout 2023.

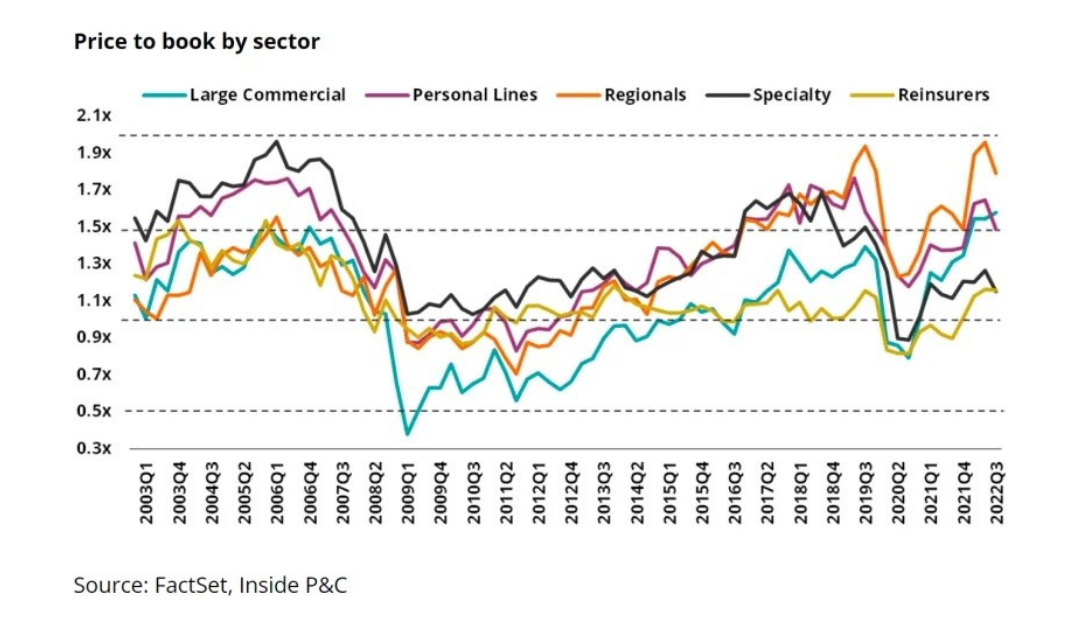

- Natural disasters: Natural disasters are one of the most anticipated liabilities affecting the instability within the P&C market environment. Wildfires, storms, floods continue to pressure the insurance industry despite efforts by insurers to temper losses by adjusting underwriting guidelines, property rates, and deductibles. In addition to complexities with financing property risks adequately, insurers are reducing capacity to satisfy their reinsures and relieve negative outlooks on their books of business from rating bureaus. Rates for CAT reinsurance increased 37% in January 2023, indicating insurers are paying excessively for coverage to mitigate risk as well as limit losses due to the anticipation for CAT in the second half of 2023.

- Evolving expectations: Lender requirements have increased in complexity and detail concerning specified requirements for limits, coverages, or deductibles. Greater coverage transparency, product availability, and pricing flexibility is needed to ease consumer fears. This is difficult to achieve in a hardening market, making a trusted agency partnership critical to navigating these complexities.

So… what can we expect? Overall, the P&C Market Outlook anticipates increased rates, minimal capacity for property, and tightly scrutinized policies. Statistically, premiums are anticipated to steadily grow to 7.5%; P&C predictions estimate that commercial property premiums will increase anywhere from 10-25%, followed by cyber at 15%, and personal lines at 13%. These trends are projected to carry into 2024 and 2025.

Despite the challenges the P&C Market is stable, resilient, and as history indicates, will emerge healthier as a result. Here are a few examples of areas where the industry is already showing signs of a healthier outlook:

- Cyber Crime: The rise of cybercrime has introduced new technologies and innovations to combat fraudulent behaviors. Incident complexity, such as in data accessibility through stealing and distributing classified information, has inspired new methods of encryption as well as complex systems that deter theft.

- AI/Cloud/Blockchain: AI, cloud, and blockchain are being integrated into business operations, ultimately improving the speed and accuracy of processes, data and information analyses, and management of internal systems.

- CAT (Catastrophic Loss): The immense influx of natural disasters has risk managers, architects, engineers and manufactures working on better risk probability indicators, design and materials to improve the integrity of insuring property in CAT prone areas. This may take time to develop and implement; however, greater adoption in one or all three of these areas will only benefit consumers and insurers alike.

So… in 2023, we can expect continued growth and innovation in technologies, a greater emphasis on customer experiences, increased adoption of AI, broader utilization of data analytics, and lingering effects from natural disasters, social inflation, and regulatory changes. As stated in the beginning of this article, the months/years ahead will likely be filled with a combination of challenges and opportunities, which at the moment feels weighted heavier on the former versus the latter.

How am I insured? What will HAWK do regarding the 2023 forecast?

Your coverage is influenced by countless factors, including but not limited to economic conditions, regulatory changes, and technological innovations. At HAWK, there are many ways we anticipate to combat any and all challenges 2023 may present. We aim to keep our clients involved and informed when it comes to assessing your insurance options.

- HAWK’s mission: HAWK’s value proposition is organized into three categories, specifically ease, options, and advice. Regardless of the environment, HAWK is dedicated to meaningful insurance and risk management decisions that support you and/or your organization in times of uncertainty.

- Curated coverage: HAWK Advisers differs from alternative insurance groups by developing strategies and coverage that best suit your needs in addition to keeps you connected with our agents.

- Independent by Nature: At HAWK Advisers, we separate ourselves from other insurance agencies by focusing on the customer experience for a seamless and transparent experience. We make sure you are always provided for by personalizing your coverage options by staying up-to-date with the latest innovations and market trends. We aspire to build strong relationships with our clients by maintaining open communication, providing quick and easy customer service, and investing in our own employee training in development, especially in times of uncertainty. We are “ALL IN”!

Despite these challenges, the P&C market remains resilient and continues to evolve to meet the changing needs of businesses and individuals. There are significant opportunities for growth in the P&C market despite the foreseeable challenges in 2023, such as the emerging developments in cyber and environmental growth. Reach out to us today so you can be one step ahead into your 2023!

Recent Comments